C2C platforms are designed to convert crude oil directly into petrochemical feedstocks such as olefins and aromatics

From "Oil & Gas" to "Energy & Chemicals". The traditional "Refinery" is transforming; the "Integrated Petrochemical Complex" is the future. Why Indian oil refining companies are aggressively pivoting toward Petrochemicals and Specialty Chemicals to hedge against the "Peak Oil" demand in personal mobility. This article presents the rise of Crude-to-Chemicals (C2C) technology and how it changes the ROI (Return on Investment) profiles of mega-projects.

The End of the Traditional Refinery Paradigm

For over a century, refinery economics were built around a single objective: maximising transportation fuels mainly petrol, diesel and ATF. Demand growth was linear, predictable, and closely linked to GDP and vehicle penetration. That paradigm is now under stress.

Electrification of personal mobility, tighter fuel-efficiency norms, and hybridisation are gradually flattening long-term growth in gasoline and diesel demand. Policy-driven energy transition measures which includes India’s net-zero commitment for 2070, aggressive ethanol blending targets, and the promotion of alternative fuels are reinforcing this trend. At the same time, demand for petrochemicals is accelerating. India’s petrochemical consumption, currently estimated at around 30–35 million tonnes p.a., is projected to nearly triple to about 80 million tonnes by 2040.

While absolute fuel demand may continue to grow in the near term, long-term growth rates are moderating, increasing the risk of margin compression and sub-optimal asset utilisation for fuel-centric refineries. Refinery risk today is less about near-term demand collapse and more about long-term relevance and capital recovery.

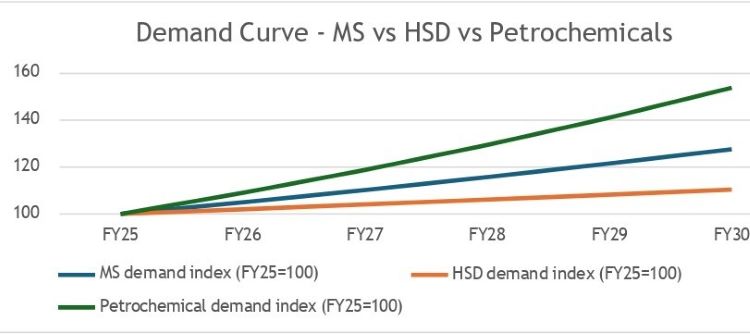

As may be seen from the figure below, MS & HSD demand growth moderates over the medium term due to electrification, biofuel blending, and efficiency gains, while petrochemical demand grows at a structurally higher pace, driven by packaging, infrastructure, and manufacturing demand.

Figure: India’s Hydrocarbon Demand Transition

Sources: Crisil Intelligence estimates

Note: Demand indexed to FY25 = 100 for illustration

Oil is Not Dying but Transforming

A critical but often misunderstood distinction in energy transition debates is the difference between oil demand and fuel demand.

While demand growth for transportation fuels has started losing momentum, demand for petrochemical feedstocks continues to grow structurally mainly on account of demand for petrochemicals from Asia region. India’s petrochemical demand, currently ~30-35 million tonnes per annum, is projected to nearly triple to ~80 million tonnes by 2040, implying a materially higher share of crude oil being directed toward chemical feedstocks.

Urbanisation, infrastructure development, packaging, consumer goods, medical applications, and advanced materials for renewable energy and electric vehicles are driving sustained growth in petrochemicals. Globally, petrochemicals are expected to account for the largest incremental demand for crude oil over the next two decades. In effect, oil is transitioning from an energy source to a materials backbone. This shift fundamentally alters how hydrocarbon assets must be designed, financed, and valued.

The Rise of the Integrated Petrochemical Complex

The response to this structural shift is the Integrated Refinery-Petrochemical Complex, a configuration where chemicals become the core value driver and fuels takes a back seat. These configurations are designed to maximise chemical yields, deploy deep-conversion units to process heavier molecules, and prioritise margin stability over throughput volumes. Integration with downstream polymers and specialty chemicals further strengthens resilience and reduces exposure to mobility-related demand risks.

This transition is already visible in Asia. China’s refining capacity has exceeded 18 million bpd, and it continues to consolidate and modernise this sector with large state-owned enterprsies like Sinopec investing in complex export oriented refineries while pursuing petrochemicals integration and regional influences through downstream investments under initiatives such as the BRI.

Closer home, IOCL is executing large integrated petrochemical expansions alongside its refining assets, notably at Paradip & Panipat. Reliance Industries has long positioned its Jamnagar complex as a deeply integrated refining-cum-petchem hub, with increasing emphasis on maximising chemical value per barrel. HPCL and BPCL are also investing heavily to expand petrochemical intensity at existing and greenfield refineries as part of their long-term transition strategy.

Why Indian Oil Refining Companies Are Pivoting Aggressively

Indian oil refining companies, historically focused on fuels marketing, are undergoing one of the most significant strategic transformations in their history. Several India-specific factors underpin this strategic pivot. India’s per-capita plastic consumption, at roughly 11 kg, remains significantly below the global average of around 28 kg, providing long-term growth visibility independent of transport fuel demand. The country also remains a net importer of several polymers and specialty chemicals, making domestic capacity creation strategically important from both an industrial policy and trade balance perspective.

From a financial standpoint, petrochemical margins tend to be structurally more stable and less regulated than retail fuel margins, improving earnings predictability. Refineries integrated with petrochemicals also enjoy longer economic lives and lower stranding risk under energy-transition scenarios. For large Indian refining companies with substantial balance sheets, deploying capital into transition-resilient assets with long-term relevance has become a strategic imperative.

Crude-to-Chemicals (C2C): A Structural Game Changer

At the frontier of this transformation lies Crude-to-Chemicals (C2C) technology. Unlike conventional refinery configurations that maximise fuels and subsequently crack intermediates into chemicals, C2C platforms are designed to convert crude oil directly into petrochemical feedstocks such as olefins and aromatics. In practical terms, this means significantly higher chemical yields, often exceeding 45% and, in advanced configurations, approaching 70–80%, with fuels becoming residual by-products.

From a project finance and investment perspective, C2C materially alters returns profiles. Higher exposure to chemicals improves average realisations per barrel and reduces earnings volatility. Asset lives are extended, capital productivity improves over the lifecycle of the project, and integration with specialty chemicals enhances strategic optionality. As a result, mega-projects that were once evaluated primarily on gross refining margins are increasingly assessed through the lens of molecule economics.

India is beginning to align with this global shift. Proposed C2C-style investments by Indian refiners, often in partnership with global technology providers, reflect a recognition that future competitiveness will depend on how effectively crude molecules are converted into higher-value chemical products.

From Energy Companies to Molecule Companies

This transformation signals a deeper identity shift. Energy companies are no longer just energy suppliers but are becoming molecule managers. Competitive advantage in the next phase will depend on feedstock flexibility, conversion depth, product-slate optimisation, downstream integration, and access to technology and R&D capabilities. In this new paradigm, success is defined not by barrels processed, but by value extracted per molecule.

Strategic Implications for Capital Markets and Policymakers

The molecule morph has important implications beyond corporate strategy. For Investors, integrated petrochemical assets command valuation premiums and offer greater resilience under energy-transition stress tests. For Lenders, diversified revenue streams and longer asset lives improve project bankability and credit quality. For Policymakers, it supports in creating skilled employment across the chemicals value chain & aligns with transition pathways without premature asset write-offs. In Indian context, it supports ‘Atmanirbhar Bharat’ and the ‘Make-in-India, Make-for-the-world’ initiatives and import substitution goals.

Conclusion: The Future Belongs to Molecules

The energy transition is not a story of hydrocarbons versus renewables but is a story of re-purposing hydrocarbons.

The traditional refinery, built for a fuel-centric world, is expected to slowly transition into the integrated petrochemical complex, powered by Crude-to-Chemicals technology, offering a future-proof pathway that balances energy security, industrial growth, and transition resilience.

For Indian oil refining companies, this is not merely a diversification strategy, it is an existential transformation.

The future of oil is not in the fuel tank. It is in plastics, polymers, performance materials, and specialty molecules. And those who master the molecule will define the next era of the energy- chemicals industry.

Subscribe to our newsletter & stay updated.